When you walk into a pharmacy to pick up your prescription, you probably don’t think about how much the pharmacy gets paid for it. But that payment - called reimbursement - is what keeps the doors open. And when a pharmacist swaps your brand-name drug for a generic version, it’s not just about saving you money. It’s about whether the pharmacy makes enough to stay in business. This is where things get complicated.

How Pharmacies Get Paid for Generics

Pharmacies don’t just get paid the same amount for every prescription. Their reimbursement comes from three main pieces: the cost of the drug itself, a dispensing fee, and sometimes a bonus or penalty based on how many generics they use. The most common system used today is called Maximum Allowable Cost (MAC). This is the highest amount a pharmacy benefit manager (PBM) or insurer will pay for a generic drug. It’s not based on what the pharmacy actually paid for it - it’s set by the PBM, often using data from wholesale prices or state Medicaid rates.

For example, if a pharmacy buys a 30-day supply of generic lisinopril for $2.50, but the MAC is set at $4.00, the pharmacy pockets $1.50 profit before even adding the dispensing fee. But if the MAC drops to $3.00, the profit shrinks. If it drops below what the pharmacy paid? They lose money. And that’s not rare. In 2023, over 40% of independent pharmacies reported losing money on at least one generic drug they dispensed, according to the National Community Pharmacists Association.

The Hidden Profit in Generic Substitution

You’d think that since generics cost less, pharmacies would make less money on them. But the opposite is often true. Gross margins on generic drugs average 42.7%, compared to just 3.5% for brand-name drugs. Why? Because the cost of generics is low, but the dispensing fee stays the same - usually $5 to $10 per prescription. That means for a $3 generic, a $7 dispensing fee gives the pharmacy a 233% markup. For a $100 brand-name drug? The same $7 fee is just a 7% markup.

This creates a strong incentive for pharmacies to substitute generics. But here’s the twist: it’s not always the cheapest generic they’re substituting. PBMs often push pharmacies to dispense slightly more expensive versions of the same drug - not because they’re better, but because they make more money for the PBM. This is called spread pricing.

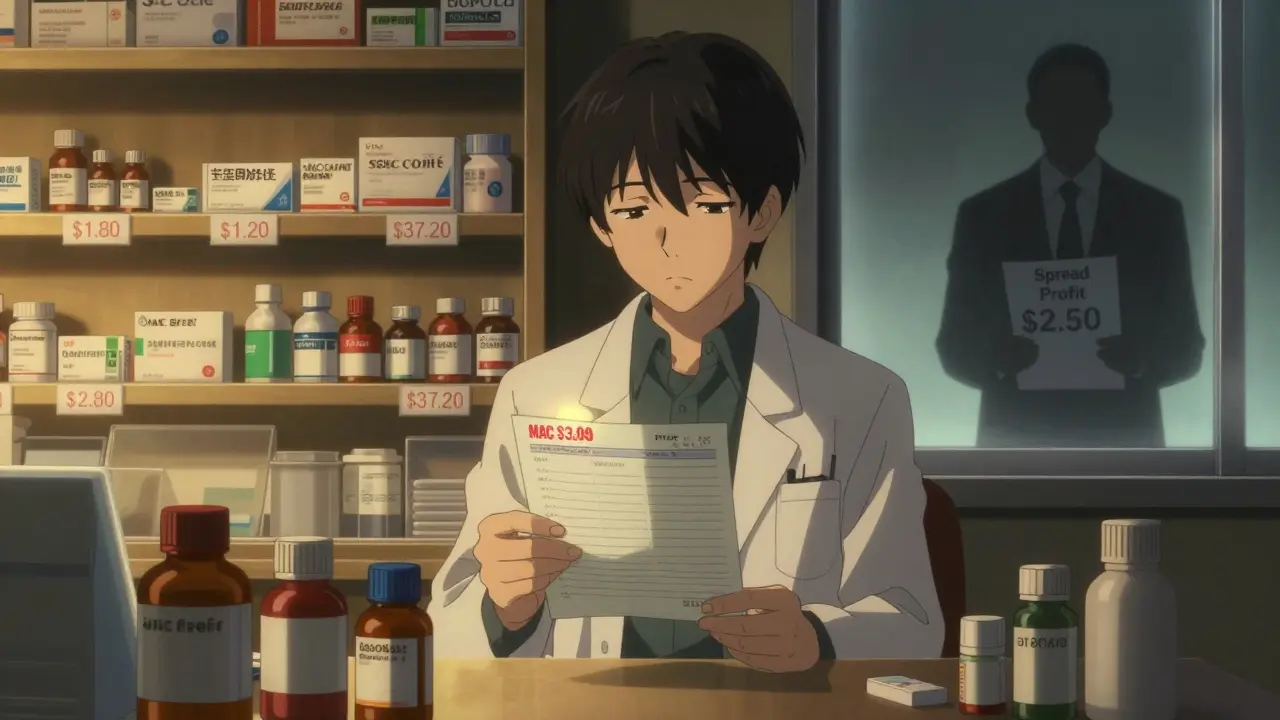

Let’s say a pharmacy buys a generic version of metformin for $1.80. The PBM tells the pharmacy they’ll be reimbursed $4.50. But the PBM charges the insurer $7.00. The difference - $2.50 - is the spread. The pharmacy gets $4.50, the insurer pays $7.00, and the PBM pockets the $2.50. The pharmacy doesn’t know the insurer paid $7.00. The patient pays their $10 copay. Everyone thinks the system is working. But the PBM made money by choosing a higher-priced generic that wasn’t the cheapest option.

Why Cheaper Generics Don’t Always Win

Studies show that the same generic drug, in the same strength, from the same manufacturer, can vary in price by up to 20 times depending on which PBM sets the MAC. One 2022 study found that when patients were switched from a brand-name drug to a generic, the price difference between the cheapest and most expensive generic in the same class was 20.6 times higher. That’s not a mistake. It’s a business model.

Therapeutic substitution - switching to a different but equally effective drug - can save even more. For example, switching from a brand-name statin to a cheaper generic statin could save $1,200 a year per patient. But PBMs rarely encourage this because it’s harder to control pricing. It’s easier to pick a slightly more expensive version of the same drug and keep the spread.

What Happens When Reimbursement Falls Too Low

Independent pharmacies are feeling the squeeze. Between 2018 and 2022, over 3,000 independent pharmacies shut down in the U.S. Why? Because reimbursement rates didn’t keep up with rising operating costs. Rent, staff wages, and compliance costs went up. But the MAC for many generics stayed flat or dropped. Some pharmacies now lose money on every generic prescription they fill.

That’s not sustainable. Pharmacies start cutting corners: reducing hours, laying off staff, or refusing to stock certain drugs. Patients end up with fewer options. If a pharmacy can’t stock a cheaper generic because the reimbursement is too low, the patient might be stuck with a more expensive brand-name drug - or not fill the prescription at all.

The Bigger Picture: Who Controls the System?

Three companies - CVS Caremark, Express Scripts, and OptumRx - control about 80% of all prescription claims in the U.S. They set MAC lists, negotiate with manufacturers, and decide which drugs get promoted. They don’t answer to pharmacies. They don’t answer to patients. They answer to insurers and shareholders.

And because they control so much of the market, they can set prices that work in their favor. A 2023 Congressional Budget Office report found that if reimbursement transparency were improved - meaning pharmacies and insurers could see exactly what PBMs are charging - average drug prices could drop 5% to 15% by 2031. But that requires changes in how PBMs operate.

What’s Changing Now?

Some states are pushing back. Fifteen states now have Prescription Drug Affordability Boards (PDABs) that set Upper Payment Limits (UPLs) - the most they’ll pay for a drug. These limits are often based on the lowest price available nationally. That means PBMs can’t keep charging inflated rates. Some states have also passed laws requiring PBMs to disclose their MAC lists to pharmacies.

The Inflation Reduction Act of 2022 started forcing Medicare Part D to reveal drug pricing data. That transparency might eventually spread to commercial insurance. If pharmacies can see what PBMs are charging insurers, they can push back. They can demand fairer reimbursement. They can stop being forced to lose money on generics just to keep their doors open.

What This Means for Patients

At first glance, generic substitution sounds like a win: cheaper drugs, lower copays, more savings. But if the system is rigged so that PBMs profit from higher-priced generics, and pharmacies are paid too little to stock the cheapest ones, then patients don’t get the full benefit. They might get a generic - but not the best one. They might pay less at the counter - but the system is still bloated.

True savings come from using the lowest-cost, clinically appropriate drug. Not the one that makes the most money for a middleman. And until reimbursement structures are fixed, pharmacies won’t be able to fully deliver on the promise of generic substitution.

Why do pharmacies sometimes give me a more expensive generic?

Pharmacies don’t usually choose the drug - the pharmacy benefit manager (PBM) does. PBMs set Maximum Allowable Cost (MAC) lists that tell pharmacies how much they’ll be reimbursed. Sometimes, the MAC for a slightly more expensive generic is higher than for the cheapest version. That means the pharmacy makes more profit on the pricier one. PBMs benefit too, because they can charge insurers more while paying pharmacies less - keeping the difference as profit. It’s called spread pricing, and it’s not always obvious to patients or even pharmacists.

Can I ask my pharmacist for the cheapest generic?

Yes, you can. Ask if there’s a lower-cost alternative in the same therapeutic class. Pharmacists can often override the PBM’s default choice if the prescribing doctor agrees. But they can’t always do it - some PBM contracts restrict what substitutions are allowed. Still, it’s worth asking. Many patients don’t realize they have this option.

Why are independent pharmacies closing?

Many independent pharmacies are losing money on generic prescriptions because reimbursement rates haven’t kept up with rising costs. Rent, staff, and compliance expenses have gone up, but MACs for generics have stayed flat or dropped. Some pharmacies lose $1 or more on each generic script they fill. That’s not sustainable. Over 3,000 independent pharmacies closed between 2018 and 2022. Consolidation is pushing more business to big chains and mail-order services, which can negotiate better terms with PBMs.

Do PBMs really make money from generics?

Yes. PBMs profit through spread pricing - charging insurers more than they pay pharmacies for the same drug. For example, if a pharmacy pays $2 for a generic and the PBM pays the pharmacy $4.50 but charges the insurer $7.00, the PBM keeps $2.50. This spread can be even higher when PBMs favor slightly more expensive generics. Studies show some generics are priced 20 times higher than their cheapest alternatives, not because they’re better, but because they maximize PBM profits.

Will transparency fix this problem?

Transparency is the first step. If pharmacies and insurers can see exactly what PBMs are charging, they can push back. Some states now require PBMs to disclose MAC lists. The Inflation Reduction Act is starting to force Medicare to reveal pricing data. Experts believe that if this transparency spreads to commercial insurance, average drug prices could drop 5% to 15% by 2031. But it won’t fix everything - PBMs still control the system. Real change needs new rules, not just more information.

Comments (15)

-

Sabrina Sanches March 12, 2026I’ve been a pharmacist for 12 years and this post nails it. Generics aren’t the problem-the system is. I’ve had patients ask why their $3 script cost them $15 when the same drug was $1.80 last month. I can’t explain it without sounding like I’m blaming the PBM. But I am. And I’m tired of losing money just to keep the lights on.

One day I stopped stocking a generic because the MAC was $0.75 below cost. The next week, the patient came back furious because they couldn’t get it anywhere. That’s not healthcare. That’s a rigged game.

-

Katherine Rodriguez March 14, 2026This is why america is broken. PBMs are just middlemen who do nothing but skim off the top. Pharmacies are getting crushed while these corporate giants get richer. No wonder independent shops are vanishing. It’s not about savings-it’s about control. And the government lets them do it. Pathetic.

-

Devin Ersoy March 15, 2026Let me paint you a picture: Imagine a guy in a suit at a desk in New Jersey deciding whether you get the $1.99 or $4.20 version of metformin. Not because one’s better. Not because it’s clinically different. Just because the spread is juicier. That’s not medicine. That’s a casino with stethoscopes. And we’re all the suckers playing slots with our prescriptions. The system is a performance art piece titled ‘How to Profit Off Sickness’ and it’s running on a loop.

Also, PBMs are the reason my grandma’s insulin costs more than her rent. I’m not mad. I’m just… profoundly disappointed.

-

Ali Hughey March 17, 2026EVERYTHING IS A LIE. 🤫

Did you know the FDA doesn’t even require generics to be 100% identical? They just need to be ‘bioequivalent’-which means the active ingredient is within 20% of the brand. That’s not the same drug. That’s a cousin. And PBMs? They’re pushing the 20% weaker ones because they’re cheaper to buy. Meanwhile, your insurance thinks you’re getting the exact same thing.

And the worst part? They’re using AI to predict which patients won’t complain. That’s not innovation. That’s predation. 🚨💉

-

Alex MC March 18, 2026I appreciate how clearly this was laid out. The disconnect between what patients think they’re getting and what’s actually happening is staggering. I’ve worked in public health for over a decade, and this is one of the most insidious examples of systemic failure I’ve seen. The fact that pharmacies are forced to lose money on generics while PBMs rake in millions is not just unethical-it’s unsustainable. Transparency alone won’t fix it, but it’s the first domino. Let’s push for it.

-

rakesh sabharwal March 19, 2026The entire US pharmaceutical ecosystem is a textbook case of market failure driven by rent-seeking behavior. PBMs function as oligopolistic intermediaries that extract surplus value through information asymmetry and regulatory capture. The MAC system, in its current iteration, is a perverse incentive structure that misaligns clinical outcomes with financial incentives. Until we implement price-based formularies with transparent reference pricing, we are merely rearranging deck chairs on the Titanic of healthcare inequity.

-

Aaron Leib March 21, 2026This is why I always tell my patients: ask for the lowest-cost generic. Most don’t know they can. Pharmacists are stuck between a rock and a hard place-we want to help, but we’re bound by PBM contracts. Still, if you push, sometimes we can override it. It’s not perfect, but it’s a small win. And yes, it’s infuriating that the system works against us. But we’re not powerless.

-

tynece roberts March 22, 2026i just got my generic lisinopril and it was like 2 bucks?? but last month it was 8?? my pharmacist shrugged and said ‘pmb did it again’ idk what pmb is but i think they’re the ones who make my meds expensive?? also i think my cat has a better drug plan than me lmao

-

Hugh Breen March 23, 2026This is why I believe in community pharmacies. They’re not just businesses-they’re lifelines. I’ve seen elderly folks walk three miles because their local pharmacy closed. And now they’re getting shipped pills from a warehouse 1,000 miles away. That’s not care. That’s logistics.

We need to treat pharmacies like hospitals-not profit centers. PBMs are not the enemy of patients. They’re the enemy of access. Let’s stop pretending this is about savings. It’s about survival.

-

Byron Boror March 24, 2026America is being gutted by these corporate monsters. PBMs? They’re not even real companies-they’re shell entities owned by big banks and hedge funds. This isn’t capitalism. It’s feudalism with a pharmacy counter. And the fact that we let this happen? That’s the real scandal. We need to burn the whole system down and start over. No compromises.

-

Rex Regum March 26, 2026Oh wow, so the system is rigged? Shocking. I guess I should’ve known when my $200 brand-name drug suddenly became a $12 generic and I still paid $15. Wait-what? That’s not a savings. That’s a trap. And now I’m supposed to be grateful? Nah. This isn’t healthcare. It’s a pyramid scheme with a white coat.

-

Kelsey Vonk March 27, 2026I’ve been thinking about this a lot lately. The real tragedy isn’t that PBMs profit-it’s that we’ve normalized it. We accept that someone else controls our access to medicine. We don’t question why the cheapest drug isn’t the default. We don’t ask who benefits. We just pay and move on. Maybe if we started treating pharmacy as a public utility instead of a commodity, we’d see real change. Just a thought.

-

Emma Nicolls March 29, 2026i had no idea this was happening. my pharmacist always says ‘this is the cheapest option’ but now im like… is it? i just asked for the lowest price and she looked at me like i asked for the moon. we need more transparency. like, real transparency. not just ‘here’s your script’

-

Jimmy V March 30, 2026The math is brutal: $7 dispensing fee on a $3 generic = 233% margin. On a $100 brand? 7%. So pharmacies are financially incentivized to push generics. But PBMs manipulate which generic they push. So the pharmacy’s incentive is hijacked. It’s a three-way game of musical chairs where the patient always loses the seat. We need to decouple reimbursement from PBM control. Full stop.

-

Richard Harris March 31, 2026Interesting read. I’m from the UK and our system isn’t perfect, but we have a national pricing structure. The NHS sets the price, pharmacies get a fixed dispensing fee, and there’s no spread. No middleman profit. Patients pay what’s fair. It’s not magic-it’s policy. Maybe we need to stop pretending this is a free market and treat medicine like a public good.